There’s a standoff happening in a lot of real estate deals right now. Buyers want relief from today’s interest rates. Sellers don’t want to gut their price. And so deals fall apart — not because the home isn’t worth it, not because the buyer can’t qualify, but because neither side has found the right lever to pull.

A 2-1 buy-down might be that lever.

It’s not a new product. But in a market where rates are elevated and sellers are finally willing to negotiate, it’s becoming one of the most useful tools in a transaction. Here’s how it works — and more importantly, how to tell if it’s right for you.

What Is a 2-1 Buy-Down?

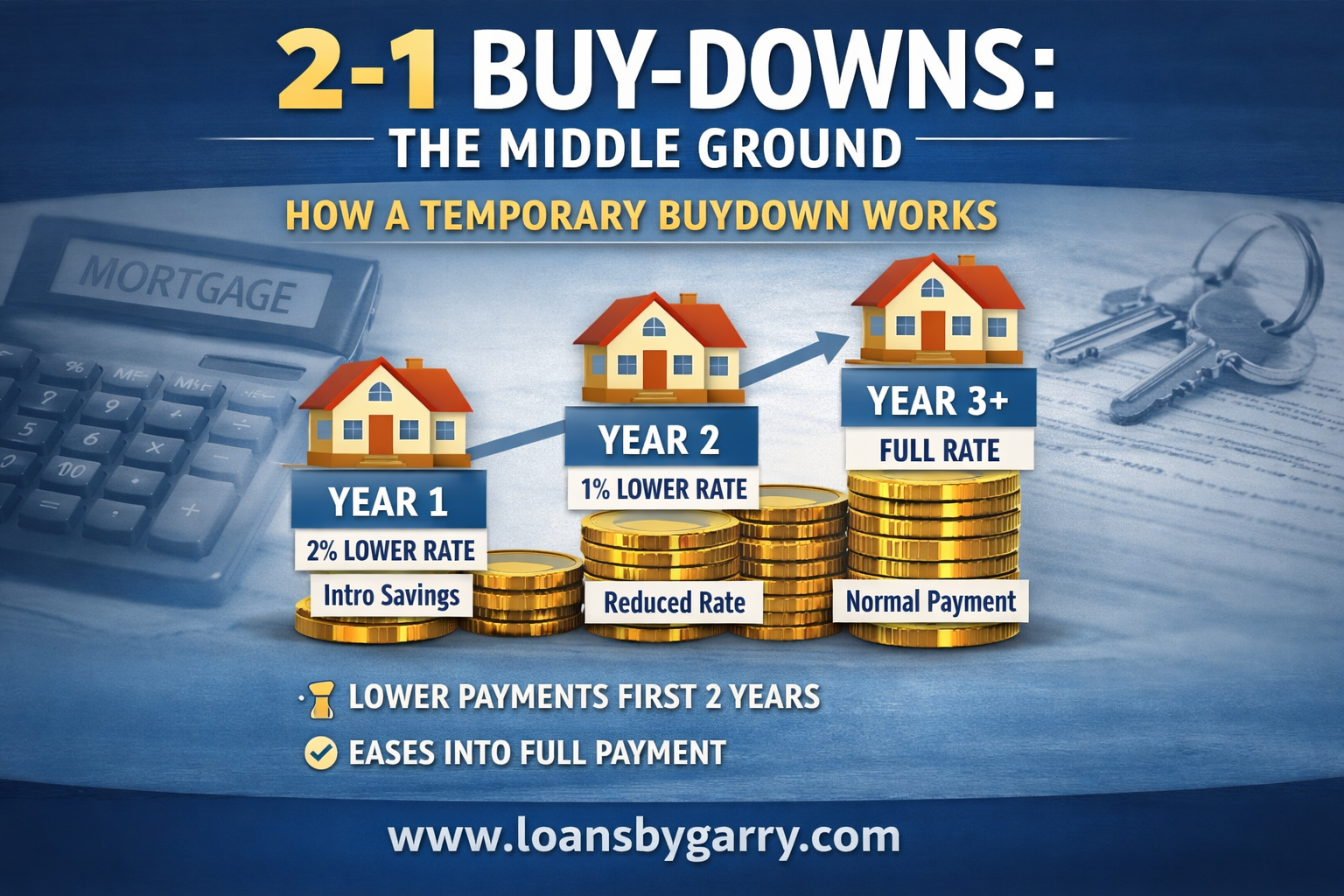

A 2-1 buy-down is a seller concession that temporarily lowers your mortgage interest rate for the first two years of the loan. After that, your rate adjusts to the permanent note rate and stays there for the life of the loan.

Here’s the structure:

- Year 1: Your rate is 2% below the note rate

- Year 2: Your rate is 1% below the note rate

- Year 3+: You pay the full note rate — forever

The seller (or sometimes a builder) funds this by depositing a lump sum into an escrow account at closing. That money is used to subsidize the difference in your monthly payment during the buy-down period. You’re not deferring interest — you’re getting a true payment reduction for 24 months, paid for upfront by the seller.

A Real Example With Real Numbers

Let’s say you’re buying a home at $650,000 with 20% down. Your loan amount is $520,000, and you’re quoted a 30-year fixed rate of 7.00%.

Here’s how your payments look with a 2-1 buy-down:

| Period | Rate | Monthly Payment (P&I) | Monthly Savings |

|---|---|---|---|

| Year 1 | 5.00% | $2,791 | $693/month |

| Year 2 | 6.00% | $3,117 | $367/month |

| Year 3+ | 7.00% | $3,484 | — |

Over the two buy-down years, you save roughly $12,720 in total payments.

Now — where does that money come from? The seller funds an escrow account at closing with approximately $12,720. That’s the cost to the seller. Instead of cutting $12,720 off the purchase price (which reduces their net proceeds AND lowers your loan basis), they redirect that money into your first two years of payments.

For many sellers, that trade-off is worth it. They protect their list price while still making the deal work.

Why This Beats a Simple Price Reduction (Sometimes)

Let’s compare the two options head-to-head. Seller wants to give you $12,720 in relief. They can do it two ways:

Option A — Price Reduction:

They drop the price by $12,720. Your loan amount goes down by about $10,176 (assuming 20% down). At 7.00%, that reduces your monthly payment by roughly $68/month.

Option B — 2-1 Buy-Down:

Same $12,720 goes into a buy-down escrow. Your savings:

- $693/month in Year 1

- $367/month in Year 2

The buy-down delivers 10x more monthly relief in Year 1 compared to the same dollar amount applied as a price reduction. If your challenge is qualifying or cash flow in the early years of ownership, the buy-down wins by a mile.

When a 2-1 Buy-Down Makes Sense for You

Ask yourself these questions:

- Are rates likely to drop in the next 1-3 years? If you plan to refinance when rates fall, the buy-down gives you breathing room until that happens — without betting your finances on a specific timeline.

- Is your income growing? If you’re early in your career or expect a raise, the buy-down aligns lower payments to your current income and higher payments to your future income.

- Is cash flow your biggest concern right now? A price reduction helps your long-term loan balance; a buy-down helps your near-term budget. Know which pressure you’re trying to solve.

- Is the seller motivated but resistant to cutting price? Buy-downs are often an easier negotiation than price reductions. Sellers feel the psychological difference between “I slashed my price” and “I helped the buyer with their payments.”

- Do you plan to stay in the home long-term? The buy-down only lowers payments for two years. If you’re planning to sell quickly, this benefit may not be worth the concession negotiation.

What to Watch Out For

You still have to qualify at the full note rate. Lenders underwrite you at 7.00% (in our example), not 5.00%. So the buy-down doesn’t help you stretch your qualification — it helps with actual monthly cash flow after closing.

The seller has to agree to fund it. Buy-downs cost real money. In a hot market, sellers won’t touch this. In a slower market or with motivated sellers, it’s very much on the table.

It’s not a permanent solution. At the end of Year 2, your full rate kicks in. Make sure your budget can handle the payment at the note rate — don’t count on a refinance that may or may not happen.

The Bottom Line

A 2-1 buy-down doesn’t solve every problem, but it solves a very specific one: it helps buyers afford the early years of homeownership when rates feel painful, while giving sellers a way to make deals happen without shredding their asking price.

In the right situation — motivated seller, buyer with growing income or a refinance horizon — it’s one of the most elegant tools in the mortgage toolkit. And right now, more sellers are open to concessions than they’ve been in years.

If you’re in the middle of a negotiation and wondering whether a buy-down could work, I’m happy to run the exact numbers for your scenario.

Garry McDonald

Loan Officer | Tried & True Home Loans

(949) 534-6686 | gmcdonald@triedandtruehomeloans.com

DRE# 01781703 | NMLS# 1922072